Barely a day goes by without an article appearing in the UK financial adviser trade press flagging up the problems associated with the investment outcomes delivered by advisers who use DFMs and model portfolios. Even the latest email from Platforum flagged a list of issues with outsourcing investment and risk profiling.

This constant drip feed of warnings and negative comment is particularly frustrating for us at PortfolioMetrix because most of the time it isn’t the fault of the financial planning and profiling done by the adviser, but rather the delivery (or lack of) by the model provider who wrecks this careful work. We are frustrated because there are good providers out there to whom none of the risks and downsides that are being flagged apply. We have purpose built our proposition to ensure we offer advisers something truly different to other DFMs and model portfolio providers – most importantly solutions that behave the way they are supposed to from a risk return separation point of view.

A recent report by The Lang Cat and reported in the FT Adviser highlighted the issues with the risk disparity present in many of the most popular funds, which is one of areas that PortfolioMetrix concentrates hardest on as part of our proposition and service to clients.

These risk deviations mean the funds can be deemed unsuitable for clients who have been risk profiled into a specific category. In many cases this leaves the adviser exposed should clients claim that the investment risk didn’t match their profile, even though the active investment is with a third party – something a lot of advisers don’t realise.

Ideally advisers should check that over time (ex-post) that their clients are getting the outcomes they expect as described during the planning phase (ex-ante).

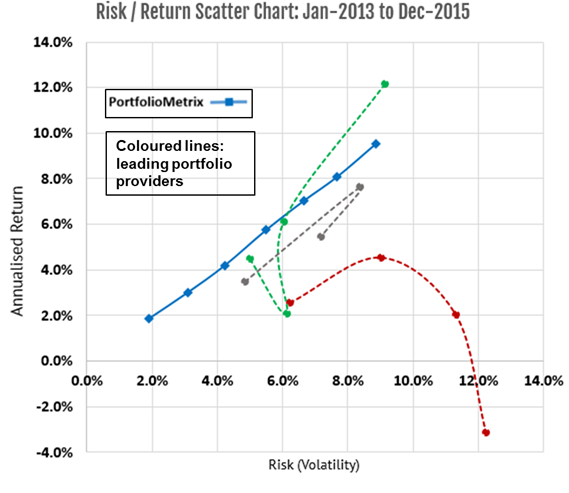

This requires plotting a sample of the investment portfolios in a risk/return scatter plot. Advisers are always promised that portfolios will line us in a nice efficient frontier shape – in a generally rising market over time clients that take higher risks will reap higher returns and vice versa. Plotting actual returns can test this promise: if the portfolios line up and produce a nice efficient frontier shape then the adviser can be confident that their investment outcomes reflect their planning and suitability process. Conversely, if, when the data is plotted, the shape, direction, spacing and consistency are not as they should be – perhaps best described as spaghetti – then there is a problem.

Admittedly, this is not a straightforward thing for advisers to do themselves whereas at PortfolioMetrix we regularly carry out this analysis. Sadly, what we’ve discovered is that the negative press coverage is true – many of the top risk-rated funds are all over the place in terms of risk separation. Given our focus on this and our robust asset allocation and fund selection process, PortfolioMetrix does not suffer from this, as our past three years of results show.

If you are an adviser who is concerned that your clients may not be getting the risk alignment you worked hard to establish as suitable for them, I’d suggest there’s never been a better time to speak to PortfolioMetrix.