No doubt your inboxes are already full of post-election commentary. There is a quick review of the results below, but our focus here is on answering the more interesting questions:

- How did the election results affect markets and the PMX portfolios?

- What might be next for the UK?

- What might be next for markets?

Election Results

It was an unambiguous triumph for the Conservatives who won with 365 seats, 47 more than their 2017 total and a parliamentary majority of 80. Also performing well on the night was the SNP, which won 48 seats, 13 more than their 2017 total. It was a disaster for Labour though, which lost 59 seats, leaving them with only 202 (some media outlets report 203, but it’s 202 if you don’t count the Speaker of the House of Commons Sir Lindsay Hoyle who, per British law, severs all affiliations with previous party), their worst result since 1935. The Lib-Dems also performed poorly, failing to make the in-roads they were hoping for and losing one seat for a total of 11.

Market Impact

Brexit wasn’t the only major driver of markets on Friday, with hints of an agreed ‘Phase 1’ trade agreement between the US and China emerging on Thursday night, the deal was confirmed later on Friday. Under the agreement, tariffs on China proposed for 15 December would not come in and those implemented in September would be halved. This undoubtedly also affected world markets positively, but for the following UK centric asset classes, the election results would have been the main driver.

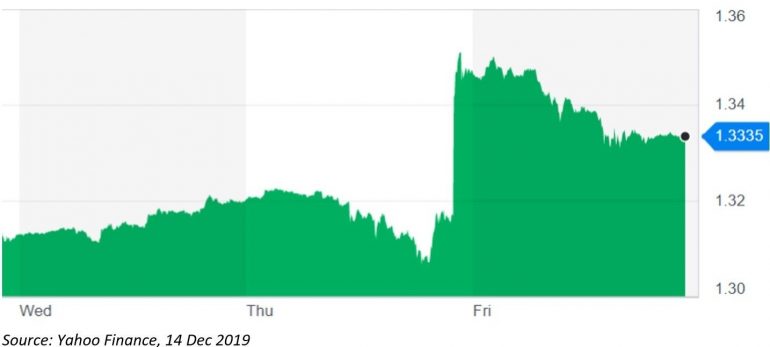

Sterling jumped briefly above 1.35 US dollars to the pound and almost 1.21 euros to the pound after exit polls indicated a likely Conservative majority, before settling down to close Friday just above 1.33 US dollars (up 1.7% using Financial Express prices) and just below 1.2 euros (up 1.4%).

The FTSE 100 was up 1.1% and the more domestically focused FTSE 250 was up 3.4% over Friday.

GBPUSD (11-13 Dec 2019)

Portfolio Impact

Over Friday, the PortfolioMetrix Select (Core Active) portfolios were up as follows:

The portfolios are carefully constructed to achieve portfolio diversification – not placing a binary bet on any election/sterling outcome.

UK holdings, about 28% of equity exposure, performed extremely strongly, up between 2% and 4.7% over the day. Pleasingly, funds selected specifically to respond positively to a lessening of Brexit uncertainty, such as Polar UK Value Opportunities (the +4.7% mentioned previously), performed as expected.

Sterling strength has been more of a problem for the value of international holdings (when measured in pound terms). This affects all overseas assets but particularly hard hit over Friday was global property which, focused on US property (with plenty of Continental European, Japanese and Hong Kong exposure) was down 2.2% over the day.

The performance of the PortfolioMetrix Select portfolios was particularly strong in the context of global equities which struggled in the stronger sterling environment: the MSCI ACWI was down 1.1% Friday in pound terms, Vanguard LifeStrategy 100% Equity was down 0.5% and previous high-flyer Fundsmith Equity (heavily weighted to the US) was down just over 1%.

Pound strength has also not just been a feature of Friday, having risen powerfully off its August lows. Over December as a whole (to end Friday) it’s up 3.2% against the US dollar and 2.1% against the euro.

Where to from here? Politics

Politically, with such a large majority of Conservatives being returned, Parliamentary gridlock will end and it’s now almost certain that the UK will leave the EU in January 2020 under Boris Johnson’s withdrawal bill. The question of the 2016 referendum was: “Should the United Kingdom remain a member of the European Union or leave the European Union?” By 31 January 2020, the will of the majority of voters in that referendum will have been carried out and, hopefully, Brexit will intrude less into the nation’s headlines and the rancour surrounding the issue will die down.

Unfortunately, this is not to say that Brexit will be ‘done’. Brexit is much more of a process than a one-off event and whilst ratifying the withdrawal bill will satisfy the 2016 referendum result, it won’t answer the key question of what the UK’s future trading relationship with the EU will be. Under the withdrawal agreement, the UK and EU have a year, until the end of 2020, to finalise a trade agreement unless an extension is sought. During this time the UK and EU will continue trading under the same conditions as exist now (as if the UK were a member of the EU).

Boris Johnson has insisted that there will be no extension and a trade deal with the EU will be wrapped up by the end of 2020. Technically, the UK could still have a hard Brexit at the end of 2020 if no free trade agreement with the EU is reached, defaulting to WTO terms. Also, the UK may try to rush through a bare bones deal with the EU in order to get it done by the end of the year. Both would seriously damage the UK economy and the market will start to focus on these risks as negotiations progress. However, with a majority of 80, 5 years left in power, a crop of new MPs representing previous Labour held seats in the manufacturing heartland of the UK (who would be hardest hit by a bad deal or no deal with the EU) and likely the majority of the UK population not paying much attention given the referendum result has been enacted, there is every incentive for Boris Johnson not to rock the boat. He can employ his flexible attitude to promises in requesting further extensions, if necessary, to do a better deal with a EU, who would also favour a deeper future trading relationship.

The second potential future political flashpoint is the future of the union. Given the SNP’s strong showing in Scotland (winning 48 out of 59 Scottish seats), Nicola Sturgeon will likely be pushing for a second Scottish referendum. Winning such a referendum isn’t a foregone conclusion, however, given the SNP vote share was only 45% (and as the most credible Remain party in many seats they may have picked up a lot of voters who don’t necessarily support Scottish independence). Equally important is that for the first time, unionist parties in Northern Ireland didn’t gain the majority of seats setting the scene for a possible referendum on Irish reunification within the next decade.

There are undoubtedly challenges ahead for the next UK government but with such a large majority, and Labour likely to be consumed with internal politics around choosing a new leader, there certainly seems likely to be more political stability going forwards than there has been over the last three years.

Where to from here? Markets

Markets don’t like uncertainty and with the result removing the chance of Jeremy Corbyn as a radically socialist Prime Minister and preventing more years of parliamentary deadlock, uncertainty in the UK has decreased. Challenges remain around negotiating the long-term UK/EU relationship and around the integrity of the UK as a whole (see above) but the outlook for Sterling and UK equities does appear brighter.

UK equities, in particular, are very cheap relative to the rest of the developed world, a post 2016 referendum phenomenon, and at least a partial retracement of this valuation gap seems quite likely.

The PortfolioMetrix portfolios already include a high weighting to UK equities (and particularly more domestically focused equities) to reflect these attractive valuations but you should expect to see further increases at the margin in future rebalances, to reflect the clearer outlook for the asset class.

That said, markets will be extremely sensitive to the chances of bad free trade agreement with the EU or a breakup of the UK, so it’s unlikely to be an entirely smooth ride for UK equities and Sterling. Also key to the performance of UK assets (and future UK interest rates and hence UK bonds) will be the extent to which pent-up investment resumes, which would revive what has this year been a particularly weak period of growth for the UK economy.