If you are using a third-party risk profiler to assess your clients’ risk appetites and an unrelated discretionary investment manager to manage the corresponding risk-profiled portfolios, you could be opening yourself and your firm up to a number of potential issues.

Why? It’s all due to an array of overlapping risk descriptions and a whole heap of assumptions. It’s easy to assume that the labels given to risk-rated investment portfolios align with those used in off-the-peg risk mapping tools. Wrong.

Risk Profiling tools are designed to measure an investor’s willingness to take risk and convert that analysis into a Risk Profile scale. These can be numbered from, say, 1 – 10 or they might be described as Cautious, Balanced, Growth or Adventurous. These scales relate to your client’s propensity to accept risk but aren’t linked to any actual investment strategy. Typically, these scales are fixed and the client, once-profiled, doesn’t move from one to another without perhaps re-running the test at a much later date.

On the portfolio side, investment management firms will often run standard risk-profiled portfolios that are also given names to describe the uncertainty inherent in these strategies. Whether these portfolios are unitised multi-asset funds or model portfolios makes no difference, there will need to be some sort of portfolio scale that describes the characteristics of each model in the range. This is where the problems start.

Similar to the descriptors used in risk-profiling tools, portfolio scales may also be numbered from 1 to 10 or they too can be written up as Cautious, Balanced, Growth or Adventurous. The key issue here is that these names relate to how the investment manager runs that range of portfolios. Again, these scales are fixed and the investment manager will adapt and change the portfolio according to the description of risk for each portfolio. This use of similar labelling for different purposes can add up to serious mis-matches.

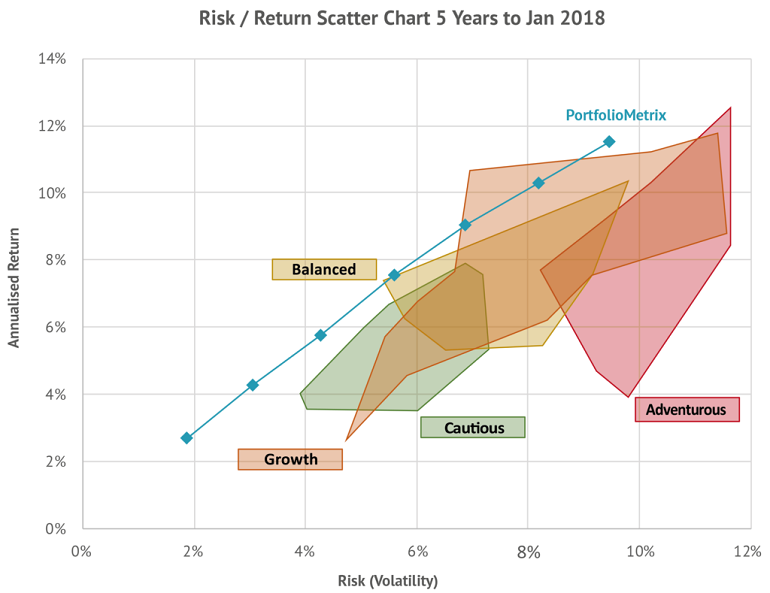

Ensuring portfolios align with clients’ risk profiles is a complex issue, which we’ve tried to explain in a paper we’ve produced (which is free to download now), entitled Risky Business: why the regulator is right to be worried about risk mapping. For the paper, we analysed the risk and return characteristics for the last five years of the 20 largest (AUM) multi-asset funds by each of the following labels Cautious, Balanced, Growth or Adventurous. The results in the table above show an alarming variation in risk/return ratios.

Aside from the obvious labelling issue, other common assumptions that can lead to issues are:

- that the volatility assumptions behind the risk profiling scale match the volatility assumptions of the portfolios

- that even if the risk profiler firm has done the mapping to the portfolios, the mapping will not degrade over time

Our paper is designed to inform you about the pitfalls of risk profiling assumptions and what you can do to help protect yourself and your clients from potentially nasty shocks in the future.

This article was first published in The Trade Press publication in June 2018.